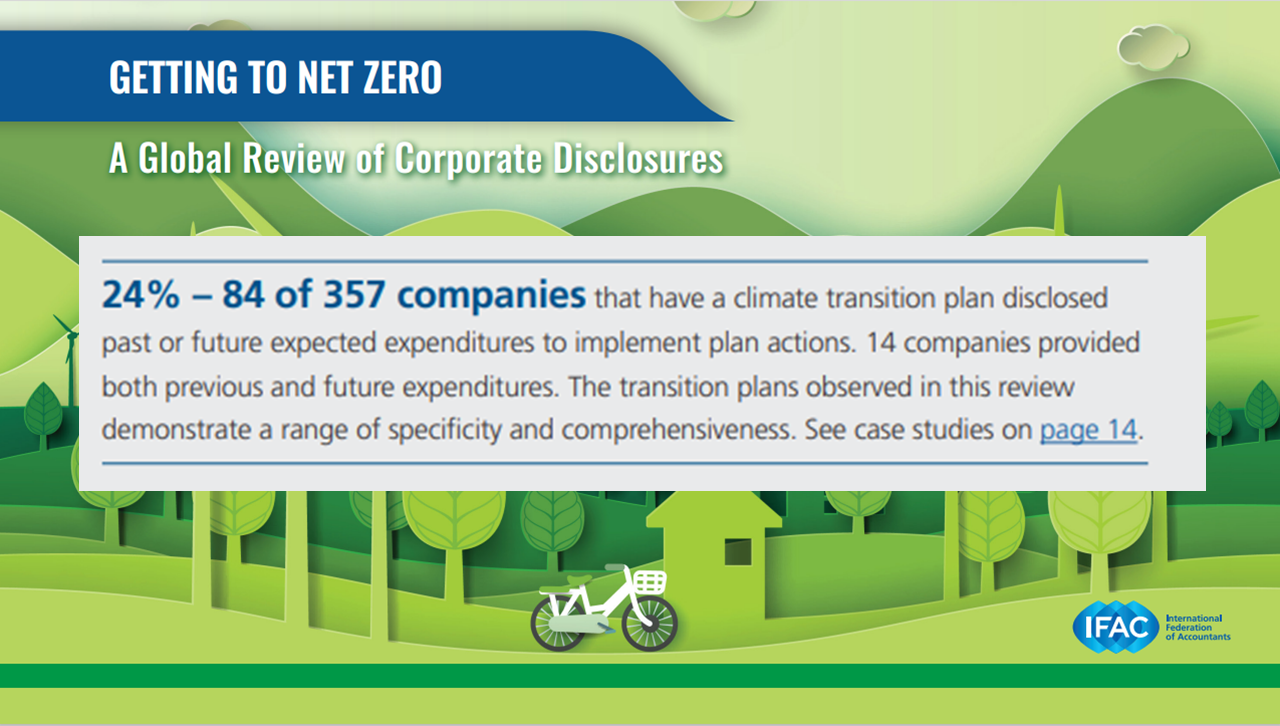

According to a recent IFAC report, only 24% of companies with plans to reduce or offset Greenhouse Gas (GHG) emissions factor in past or future expenses for implementing those plans. This suggests that 76% of companies are pretty much flying blind when it comes to the costs of executing plans to reduce emissions, we want to solve that.

To address this, we kicked-off the reinvigorated Environmental Sustainability Interest Group (ESIG) at the CAM-I quarterly meeting on March 6-7, 2023.

The group’s primary objective is to develop solutions to help organizations transition to a greener business model in a financially sustainable way.

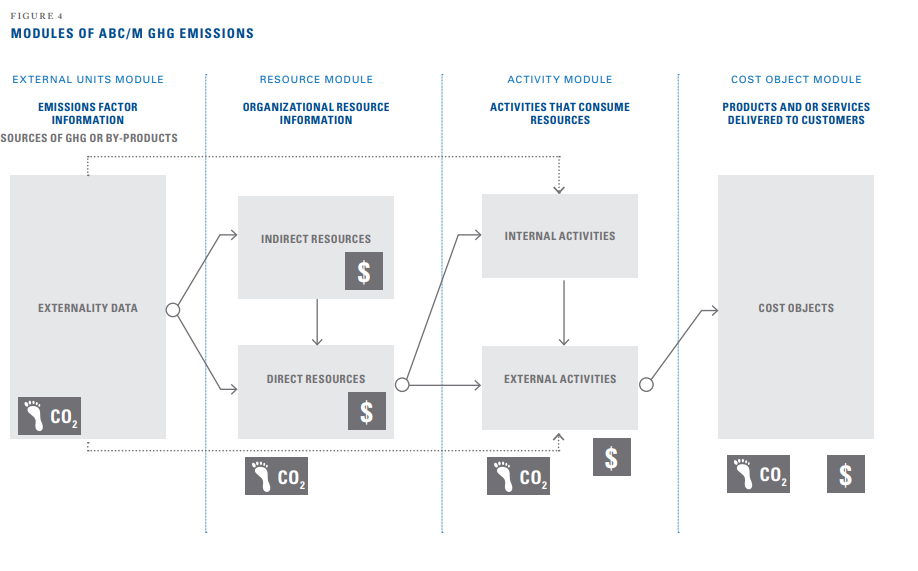

As previously mentioned, the ESIG is an Interest Group of CAM-I, a non-profit organization dedicated to developing collaborative solutions in various areas such as cost, risk, process, supply chain, and environmental sustainability. CAM-I will be celebrating its 50th anniversary this year, and for those familiar with Activity-Based Costing (ABC), you may have come across the CAM-I Cross which was developed by CAM-I in 1990.

Over ten years ago, we established the ESIG and produced a whitepaper with contributions from Grant Thornton US, CMA Canada (Now CPA Canada), International Federation of Accountants, Boeing, Weber State University, SAS Institute, and Dresser-Rand (now Siemens Energy). Our goal was to create a methodology that integrates financial and environmental costs into a single model. Unfortunately, the approach, which we believed was a no-brainer, did not generate much interest.

Fast forward ten years, and carbon accounting solutions and consultancies have become ubiquitous. It seems that every time I read the news, there is another venture capital-funded carbon accounting software product on the market. While I believe it’s fantastic that there is so much interest now, the problem with treating carbon accounting in isolation is that it’s not integrated into an organization’s long-term planning and strategy. Instead, it’s mostly used as a tool to fulfill external reporting requirements, which are currently mostly voluntary.

However, the CAM-I methodology can work in collaboration with carbon accounting firms and software products as the emissions data needs to come from somewhere. The value that the CAM-I methodology provides is that it links emissions to financial costs and the operations of an organization through resources, activities, and ultimately allocated to individual products/services. By including revenue, an organization can report cost, profit, and emissions on a per product/service basis to support strategic planning and allow for a financially sustainable transition to a greener business model.

The reinvigorated ESIG now comprises representatives from CPA Canada, Cherry Bekaert, King County (Washington State), Indiana University, and we were honored to have Professor Karthik Ramanna from the e-liability institute present at our meeting. The e-liability methodology, co-developed by Professor Ramanna (Oxford University) and Robert Kaplan (Harvard University), was discussed during the meeting.

e-liability

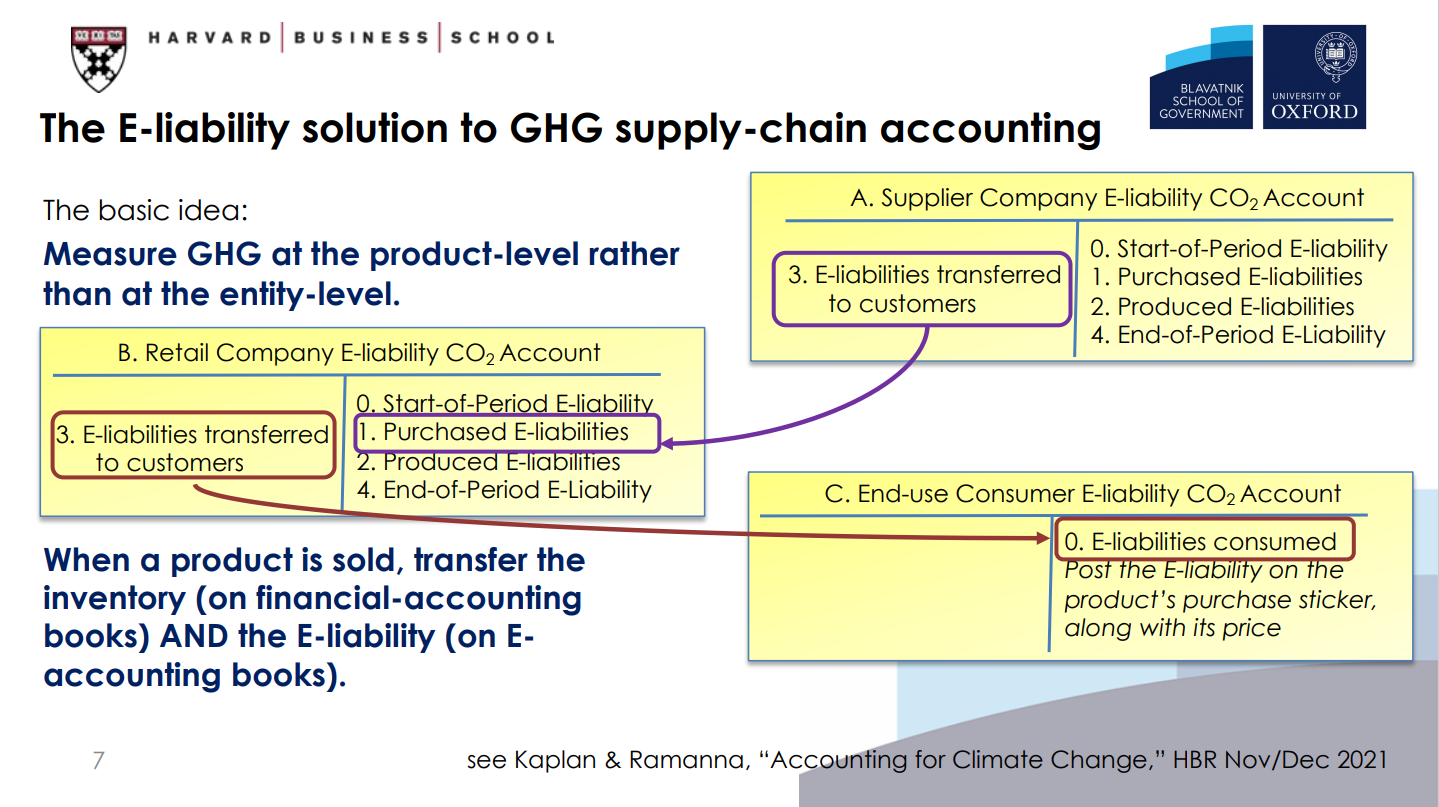

The e-liability methodology was specifically developed to address two main issues with scope 3 accounting:

- Inaccurate – Under current standards it’s very difficult to collect supplier specific scope 3 data, therefore organizations choose industry averages, which results in guestimates and gaming of GHG accounts.

- Multiple counting of emissions along the value chain – A product with ‘n’ entities in its supply chain will have its emissions (and offsets) counted ‘n’ times.

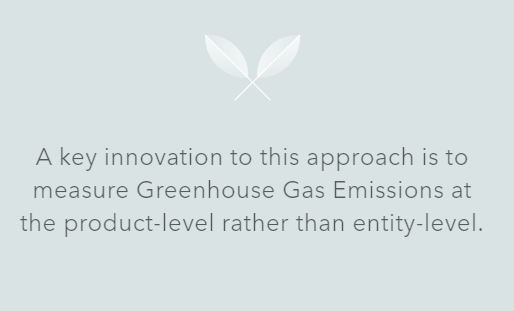

During the meeting, Professor Karthik emphasized that any accounting system developed needs to accurately count everything material and only once, which is precisely what the e-liability methodology has been designed to accomplish. He also highlighted that the key innovation of this approach is measuring emissions at the product level, which is perfectly aligned with the CAM-I methodology. I would add that another significant innovation of the e-liability approach is sharing product-level emissions on a distributed ledger, such as blockchain, rather than being tied to any central system.

The ESIG is excited to collaborate with the e-liability institute and is currently evaluating several potential organizations to implement pilot models and use them as case studies. The two methodologies should work seamlessly together, with GHG emissions being measured at the product-level instead of the entity level. Then, when the product is sold, the inventory (on financial accounting books) and the e-liability (on e-accounting books) can be transferred. The emissions can be recorded on a blockchain with third-party assurances, allowing for verifiable transmission of emissions across supply chains.

The CAM-I ESIG methodology can integrate with this approach by utilizing the ABC component to calculate emissions at the product-level while also including financial cost information, which can support internal management and strategic planning.

Higher Education

This methodology is certainly relevant to Higher Education. In fact, we have already developed a pilot model at Weber State University and one of our Australian client universities has already started incorporating environmental metrics into their model. Additionally, there is an organization called Second Nature that is committed to accelerating climate action in, and through, higher education.

If your institution has a Sustainability team or Environmental Sustainability is a part of your strategic plan, please feel free to share this post. If your organization already has our cost model in place, it is relatively simple to integrate GHG emissions into your model as long as you have access to the necessary data, either from your sustainability team or an existing carbon accounting software.