Financial analysts use a wide range of cost allocation methods, including cost per student credit hour, in universities to calculate the cost of delivering courses and programs. I will show you why this is fraught with danger and could cause more harm than good!

In recent posts I have used data from our Australian demonstration model however in this post I will use the US demonstration model and in particular using Student Credit Hours as a basis for allocating costs.

Student Credit Hours

The Student Credit Hour seems to be ‘the’ go-to metric for cost allocation for financial analysis of courses and programs, unfortunately it can be horribly misleading. Costs should be allocated based on the level of effort required to teach and support the course, this means calculating the Academic Workload. I know, I can hear your concerns already “we don’t run timesheets” and “it’s way too much effort to survey staff” and these are both valid arguments. But there are ways of doing this easily and successfully, however before we get into this, let’s take a look at why this is a problem.

Full Cost of Academic Programs

Calculating the full cost of Academic Programs is hard! To start with there is no simple report that can be pulled out of the financial management system that shows this cost. The full cost is calculated based on data from multiple systems:

- Financial – Actual expenditure

- HR/Payroll – Who the teaching staff are, their level (professor, adjunct etc) and how much they are paid

- Timetable – Which classrooms are used

- Facilities – Costs associated with classrooms – maintenance, utilities, depreciation

- Student Management – Numbers of students in each course, types of revenue

Collecting, cleansing and transforming all of this data is a significant job, and connecting the dots between all of these systems is even more complex. But this only addresses DIRECT cost. The next step is to allocate all the OVERHEAD (IT support, HR Support, Student Management etc.) – this increases the level of effort exponentially. To properly allocate overhead you need to build an Activity-Based Costing model (after all this is why Activity-Based Costing was developed in the first place back in the mid-1980s). If you don’t have the expertise or time to do this, what do you do?

Direct Cost of Academic Programs

Direct cost is good enough for School/Department level operational management and with a subset of data from these various systems this analysis can be undertaken in a spreadsheet. But once we have the data from the various systems, how do we allocate these costs to Programs? Firstly the costs need to be allocated to where the work is undertaken – at the course level, this is where the teaching effort and student support actually occurs.

Then these courses must be allocated to the programs they support, but this starts to get a bit tricky as well because it’s actually a many-to-many relationship between Programs and Courses. What does this mean? It means that:

- A Program can have multiple Courses associated with it

- A Course can have multiple Programs associated with it

Let’s take this one step at a time. Firstly, how do we do the first stage of the allocation of costs to courses? Each component of cost would be allocated in different ways – as an example maintenance and utilities can be allocated to specific classrooms based on the size of the classroom (data from the facilities system). The biggest expense by far is salary, so how best to allocate this cost? When it comes to work performed by people, the best way to divide the cost of that person is to work out how much time they spend doing the various tasks they do. Unfortunately, timesheets are not used at universities and the last thing we want to do is survey the staff.

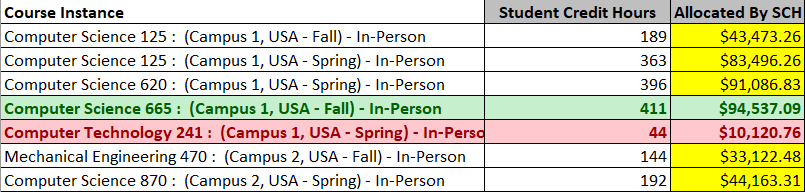

The next best option is to use some type of proxy metric – the Student Credit Hours – this should provide a reasonable representation of level of effort. So let’s take a look at some actual numbers.

I’ve taken a sampling of courses from our demonstration model and from the School of Engineering and Computer Science. These courses were specifically chosen because they cover a nice range of different sizes and levels of effort.

For ease of calculation the total cost that needs to be allocated is $400,000.

Option 1: Cost Calculations based on Student Credit Hours

This allocation method is very simple, the $400,000 is distributed to the course instance using the ratio of SCH.

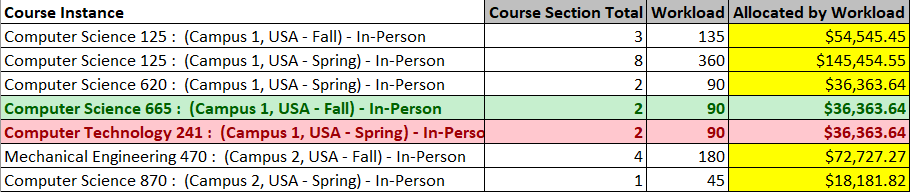

Option 2: Cost Calculation based on Workload

The workload calculation in this example has been kept very simple on purpose, so that it’s easy to calculate and understand.

Quite simply, all I have done is estimated a workload of 3 hours per week per section. Using 15 weeks per semester, we have 45 Hours per Semester per Section.

SCH vs Workload

Now we have the results of the two calculation methods, let’s compare the different costs.

The first thing to notice is that there are some very distinct differences in the cost calculated.

Some things are self-evident when you look at the data using the workload allocation method:

- The bigger the class size the more cost effective the teaching.

- Vice-versa, the smaller the class size the more expensive.

You can easily see this in the “Cost per SCH by Workload” column – the class with an average section size of 69 (Computer Science 665) is only $88.48 per SCH compared to $826.45 for the class with average section size of 6 (Computer Technology 241)

But smaller class sizes may lead to a higher quality learning experience – this is a trade-off decision to be made by Academic staff – but you need the real data to enable proper trade-off decisions to be made.

This means that when looking at the allocation by Student Credit Hours we can see that it is distorting this by:

- Underestimating small class costs,

- While Overestimating large class costs.

Academic Workload

As mentioned previously the Academic Workload in this example was kept purposefully simple. In our actual models we would include a range of metrics including time for:

- Preparation

- Marking

- Supervision

- Assistance

- Administration

We would also differentiate all of these for different teaching methods, so online workloads would be different to In-Person workloads.

So how are we able to collect all this workload data without burdening academic staff? Because we have the data already!

We have a wide range of workload data for a large number of courses across multiple institutions, multiple years and multiple countries, so we can start with some standard profiles we’ve developed. But this is just the starting point, the models we develop are enduring models (they grow and evolve with the institution) and they are “management by exception” models. That is, we start with the standard profiles and if a school/department or even an individual Academic doesn’t like them, then they can easily change them. It might take a few iterations to get something that the institution and academics are happy with, but it’s done over time and with the ability to see the results of the changes as well. In fact, if you wanted, you could run multiple different scenarios and compare different workloads and look at the resultant changes in cost.

While using Student Credit Hours seems like a logical and time saving way of allocating cost, you can easily see that this can distort the estimated costs to teach, therefore leading to decisions that could hurt the institution more than help.