Today’s post comes from our good friend at Arkonas, John Miller. With 40 years experience both in industry where he held the position of CFO for a publicly held New York Stock Exchange company and as a principal to industry for an international consulting firm, John combines the skills of a consultant with the mindset of a CFO. John is a frequent and featured speaker at international and domestic conferences, seminars, summits, and training events. A prolific author, John has published over 50 articles, papers, and books.

Today’s post comes from our good friend at Arkonas, John Miller. With 40 years experience both in industry where he held the position of CFO for a publicly held New York Stock Exchange company and as a principal to industry for an international consulting firm, John combines the skills of a consultant with the mindset of a CFO. John is a frequent and featured speaker at international and domestic conferences, seminars, summits, and training events. A prolific author, John has published over 50 articles, papers, and books.

This post is a general introduction to Activity-Based Costing (ABC). ABC is a powerful methodology and is the fundamental thinking underlying our Cost Wise College modeling. We have taken the basic ABC and enhanced it to provide a more sophisticated and automated model, saving time, money and manhours in building and maintaining the model.

Please enjoy John’s overview.

ACTIVITY-BASED COSTING

The roots of Activity-Based Costing (ABC) go back almost 100 years. In 1919, the earliest know reference to ABC, Dexter S. Kimball Professor of Industrial Engineering and Dean, College of Engineering, Cornell University published Cost Finding. Dated in terms of examples (in 1919 the fully burdened direct labor rate was 38 cents an hour), the emphasis was on activity costing and accounting for activity cost, activity output, and activity performance.

In 1971, George J. Staubus, Professor of Business Administration at the University of California Berkeley, published Activity Costing and Input-Output Accounting. Again the focus was on activity costing and accounting.

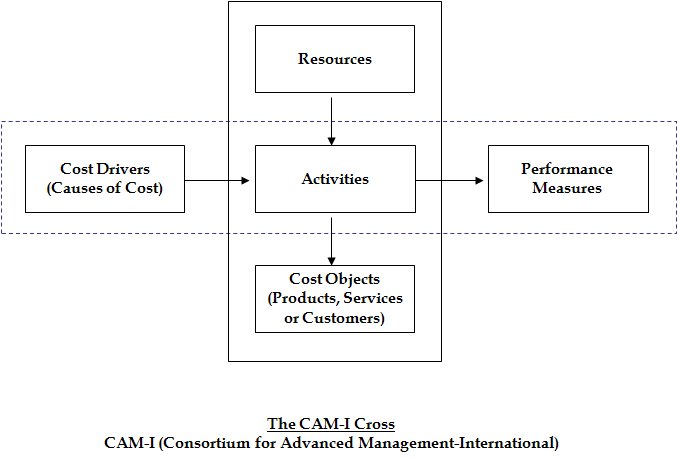

In 1988, CAM-I published Cost Management for Today’s Advanced Manufacturing: The CAM-I Conceptual Design.

The concepts included the ABC two-stage cost assignment methodology where resources (costs) are first traced/assigned to activities (work) and the resultant activity costs are then traced/assigned to products, services and customers (cost objects).

Known as the CAM-I Cross, the focus of ABC was no longer just activity costing and activity accounting but rather a tool for cost analysis, profitability analysis, and performance measurement.

SAP, SAS, IBM and other Enterprise class software providers recognized the power of ABC and acquired most of the standalone ABC software providers between 2002 and 2006, embedding ABC in their suite of products with a broader emphasis on performance excellence and management.

Today, ABC is more of a best practice for cost assignment, included in projects for product /service profitability analysis, process improvement, shared service charge back, customer profitability or even for vendor analysis.

ABC has been around for 100 years because it is aligned with the basic mission of any commercial organization: convert resources to products and services customers want to buy. Resources fund the activities (work) required to make and provide products and services to customers. Activities are the means of conversion, the so called “value add” by the business.

Improve you analytical capability. Know your ABC’s

John A. Miller